About the article

DOI: https://www.doi.org/10.15219/em112.1735

The article is in the printed version on pages 67-74.

Download the article in PDF version

Download the article in PDF version

How to cite

Alińska, A., & Olczak, A. (2025). Pocket money and financial socialisation: students’ spending behaviours and experiences. e-mentor, 5(112), 67-74. https://www.doi.org/10.15219/em112.1735

E-mentor number 5 (112) / 2025

Table of contents

- Introduction

- Methodology

- The Essence and Functions of Pocket Money

- The Influence of Pocket Money on Financial Attitudes – A Review of Studies

- Pocket Money and Financial Education at the Higher Education Level

- Pocket Money in Students’ Experiences – Results of Own Research

- The Impact of Pocket Money on Saving and Spending Planning Among Youth

- Perceived Financial Risks and Challenges

- Summary and Discussion of Research Results

- References

About the author

Pocket Money and Financial Socialisation: Students’ Spending Behaviours and Experiences

Agnieszka Alińska, Anna Olczak

Abstract

The challenges of the modern economy require young people to possess increasingly advanced financial competencies and the ability to manage their own financial and economic resources. This article attempts to analyse the role of pocket money as a tool supporting the process of students’ economic education. It is assumed that the regular receipt and independent management of pocket money help young people develop financial responsibility, budgeting skills, and an awareness of the value of money. The study aimed to identify the relationships between the amount and spending patterns of pocket money and students’ level of financial independence, as well as their prior family experiences. The research employed a questionnaire survey conducted among 180 first-year students from both economic and non-economic majors, complemented by a structured narrative review of domestic and international literature. The results indicate that pocket money plays a significant role in shaping the economic competencies of young adults, and its importance increases during the transition from financial dependence on parents to economic independence. A well-designed practice of providing pocket money can serve as an effective element of early financial education, preparing young people for rational personal financial management in adult life.

Keywords: economic education, pocket money, financial competence, economic independence, students

Introduction

The dynamic and complex structure of today’s economy places increasingly high demands on young people in terms of economic competence. The ability to manage one’s personal finances is not only an essential skill for independent living but also a crucial factor influencing decision-making in areas such as entrepreneurship and the allocation of accumulated savings for investment purposes. Many individuals still lack adequate knowledge and understanding of effective and proper personal financial management. As a result, they are unable to plan and control their expenses in ways that support the achievement of long-term life goals (Novianti & Kurnia, 2023).

Economic education, both in Poland and worldwide, is recognised as one of the key components of general education, and its effectiveness largely depends on the influence of the family, the first environment for financial upbringing. A commonly used method of family-based financial education is pocket money, defined as the regular practice of giving children, adolescents, or students financial resources to cover their daily needs, such as food, clothing, or entertainment.

This article examines students’ experiences and opinions regarding the role of pocket money in their financial education. The study hypothesises that pocket money serves as an important tool for developing students’ financial independence. Attention was given to the relationship between students’ opinions about pocket money and their family experiences, such as household income levels and parenting practices. As part of this analysis, a closed-question survey was conducted among 180 first-year regular studies students from both economic and non-economic programmes, and a systematic review of the literature was carried out. The analysis of the collected data provides a deeper understanding of how childhood and school experiences influence students’ current financial attitudes, knowledge, and money-management skills.

Analysing pocket money among students is particularly important, as this social group stands on the threshold of economic independence and will, in the future, make decisions regarding the structure of household budgets. The period of higher education marks a transition from financial dependence on parents to gradual independence, and it is during this time that financial habits formed in earlier stages of life are tested in practice. A high level of financial competence among students translates into rational decision-making regarding expenditures, student loans, part-time work, and investments in professional development (Lusardi et al., 2010).

Methodology

The study used a questionnaire-based survey administered to 180 first-year students in economics-related and non-economics programmes. The research instrument was a structured 30-item questionnaire. The questionnaire consisted mainly of closed-ended items, including several rating-scale questions, most of which used a five-point Likert scale (1–5), along with one ranking question. The questions addressed issues related to pocket money, including its amount, frequency, how it was spent, and students’ perceptions of its role in their financial education to date.

A purposive sampling approach was used, focusing on first-year university students, as they had relatively recent experience with receiving pocket money. Additionally, this group is often in the early stage of transitioning to greater financial independence, which may influence their perceptions and attitudes toward pocket money. Participants were recruited from universities in Warsaw due to the researchers’ accessibility to this population. The empirical study was complemented by a structured narrative review of domestic and international literature.

The Essence and Functions of Pocket Money

Pocket money refers to the regular financial allowance given by parents or guardians to children, adolescents, or students to cover their personal, everyday needs such as food, clothing, entertainment, or small purchases. It serves as an early form of financial socialisation, introducing young people to concepts such as money management, budgeting, and decision-making about expenditures. As emphasised by Laily, pocket money serves as a means of fostering responsibility and as an educational tool for students to manage their finances effectively (Laily, 2016). Pocket money provides young people with an opportunity to develop a sense of independence and responsibility while simultaneously learning the consequences of their financial decisions. From an economic perspective, pocket money can be considered a micro-model of personal financial management, through which young individuals acquire basic experience in budgeting, saving, and spending. This process aligns with the concept of financial literacy, understood as the ability to make informed financial decisions based on knowledge and skills (OECD, 2016).

Pocket money, as one of the first financial experiences of young people, serves a range of functions that can be analysed from social, educational, and economic perspectives. Having one’s own money and the ability to spend it according to personal needs forms the basis of its social function, as it allows young people to meet their needs and participate in social life (e.g., going to the cinema, engaging in sports, pursuing hobbies). Regular receipt of pocket money promotes social integration and fosters a sense of belonging to a group (Webley & Nyhus, 2006).

At the same time, pocket money is an element of the economic socialisation process, through which young people learn norms and values associated with possessing and spending money (Shim et al., 2010). Its educational function primarily relates to developing the skills needed to manage limited financial resources. Pocket money provides opportunities for practical financial learning, including budgeting, comparing prices, saving, and making consumption choices (Bucciol & Veronesi, 2014). From an educational standpoint, it represents a form of ‘learning by experience’, allowing young individuals to acquire economic knowledge in a natural and comprehensible way.

The financial function of pocket money involves introducing the basic mechanisms of money management, helping young people recognise its value and significance. Early and regular contact with money, for which they are responsible, enables an understanding of economic processes at both micro- and macro-levels, forming the foundation for future financial competencies. As Lusardi and Mitchell (2014) note, experiences from childhood and adolescence have a significant impact on the level of financial literacy in adulthood.

The Influence of Pocket Money on Financial Attitudes – A Review of Studies

Empirical research on the significance of pocket money for shaping financial attitudes has been conducted since the 1980s. Early studies by Furnham (1999) demonstrated that children who regularly received pocket money were more likely to exhibit pro-saving behaviours and higher financial awareness compared to their peers without such experience. Similar results were reported by Webley and Nyhus (2006), who found that both the amount and frequency of pocket money received correlated with a greater tendency to save in adulthood.

More recent studies, however, indicate a more complex nature of this relationship. Bucciol and Veronesi (2014) emphasise that the impact of pocket money on financial attitudes is mediated by the method of distribution–particularly whether parents use it as an educational tool (accompanied by discussion, explanation, and spending supervision) or treat it as an unconditional allowance. In the latter case, the educational effect may be limited, and young people may develop more impulsive spending behaviours.

Moreover, research by Shim et al. (2010) showed that early financial experiences, including receiving pocket money, significantly impact students’ financial competencies. Individuals who managed their pocket money independently during childhood showed a greater propensity for budgeting, avoiding debt, and making rational financial decisions.

Some studies also highlight the importance of cultural and social context. Lozza (2023) notes that in societies with high levels of consumerism, regular access to money can lead to materialistic attitudes and impulsive purchasing decisions if it is not accompanied by financial education. This underscores the necessity of integrating the practice of giving pocket money with systematic instruction in personal finance.

Contemporary empirical research on the impact of pocket money yields mixed findings. Some studies point to positive effects, such as increased financial awareness, responsibility, and planning skills (Shim et al., 2010), while others suggest that regular access to money without the appropriate educational context, close parental involvement, or sufficient economic and financial knowledge may encourage the development of consumerist and impulsive spending behaviours (Lozza, 2023). These differences often result from variations in social and cultural models, as well as the level of educational support provided by families and educational institutions.

It should be noted that a family’s economic status and the parents’ level of education are among the key factors differentiating both the amount and regularity of pocket money provided. Research conducted by Furnham (1999) showed that parents with higher financial standing – most often middle class – are more likely to give their children regular, consistent pocket money. The author emphasises that in such households, financial support for children is perceived not only as part of maintenance but also as an instrument of economic education, enabling them to learn budgeting, independence, and responsibility for their own spending decisions.

Pocket Money and Financial Education at the Higher Education Level

In the context of higher education, pocket money can be viewed as one of the formative factors shaping students’ early financial competencies. The university period marks a transition from financial dependence to independence, during which young adults begin making decisions regarding employment, saving, and credit. As noted by Lusardi, Mitchell, and Curto (2010), the level of financial literacy among students directly affects their ability to manage resources effectively, while earlier economic experiences – including the management of pocket money – are significant predictors of these competencies.

From a didactic perspective, analysing the phenomenon of pocket money among students can contribute to a deeper understanding of how economic competencies are acquired in practice. The literature emphasises that traditional, theory-based economic education is less effective without a practical component that allows students to learn through real-life experience, particularly in the area of personal finance management (Mandell & Klein, 2009). In this sense, pocket money can be seen as a form of ‘learning by doing’, fostering both financial independence and economic responsibility.

In an era of increasing financial market complexity and easy access to consumer credit, early economic experiences have gained even greater significance. Examining the relationship between the amount and frequency of pocket money received and students’ levels of financial competence may help develop more effective educational strategies, both within families and in academic programmes.

Pocket Money in Students’ Experiences – Results of Own Research

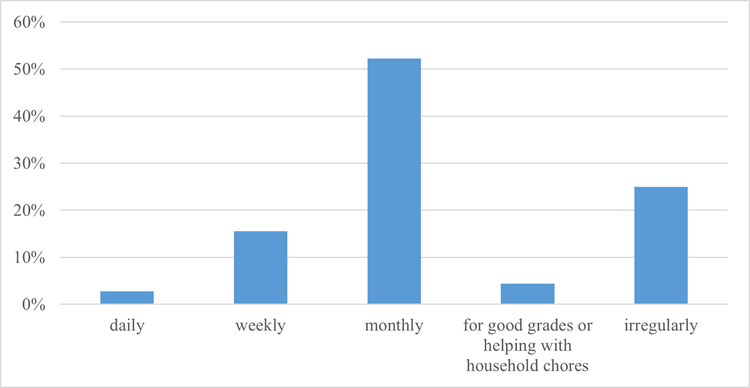

Pocket money is a widely practised form of financial support and an element of economic upbringing within households, aimed at teaching children and young people basic financial responsibility. According to the conducted survey, the vast majority of students reported having received pocket money during their childhood – 156 out of 180 respondents (86.6%) declared that they had received pocket money, while only 24 respondents (13.4%) stated that they had never received regular financial allowances from their parents or guardians (Figure 1). Most of the surveyed students received pocket money on a monthly basis (94 responses).

Figure 1How often did you receive pocket money?

Source: authors’ own work.

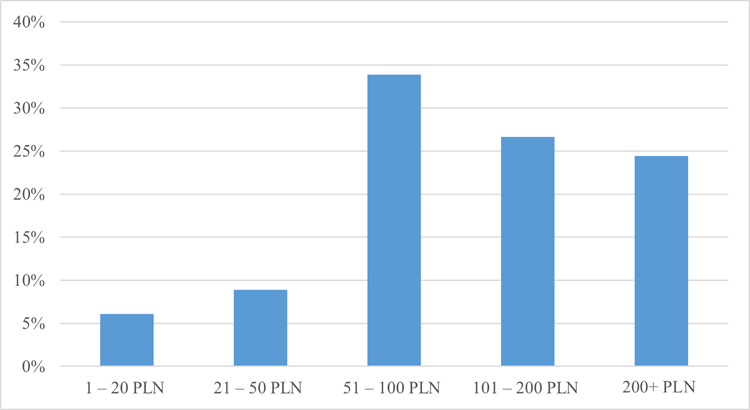

The most frequently reported ranges of received pocket money were PLN 51–100 per month (61 respondents) and PLN 101–200 per month (48 respondents – 26.6%). The majority of participants considered the amount they received to be sufficient for their needs (136 out of 180 respondents). A total of 97 students (53.8%) indicated that the amount of pocket money they received was fixed, while 83 respondents stated that it depended on certain conditions – most often academic performance or involvement in household duties (Figure 2).

A clear majority of students (160 respondents – 88.8%) also admitted that, in addition to regular pocket money, they occasionally received extra funds for specific purposes, such as going to the cinema or meeting with friends.

The relatively modest sums of money received regularly by young people beginning their university studies may reflect established norms and the specific organisation of household finances in individual families. However, it is difficult to agree with the observed notion that a monthly allowance of around PLN 100–200 would be sufficient to cover living expenses in a university city. Student expenditures are typically much higher and differ significantly from the financial needs experienced during secondary education.

This situation suggests that students who do not work are often treated as dependent household members, with most of their financial needs and living expenses being covered directly from their parents’ budgets, rather than from personal income or savings.

Figure 2How much pocket money did you receive?

Source: authors’ own work.

The level of spending on pocket money varies depending on household characteristics. In 2015, expenditures on pocket money were higher in rural households than in urban ones. The highest levels of such spending were recorded in households of farmers and manual workers, as well as in those where the head of the household had a relatively lower level of education.

The share of pocket money in total household expenditures has been systematically increasing, which, from the perspective of developing financial awareness, can be regarded as a positive phenomenon. As emphasised by Piekut (2018), this may indicate not only an improvement in the financial situation of Polish households but also a growing awareness of the importance of allowing young people to manage money independently.

The results of the conducted survey show that the majority of respondents (103 out of 180 – 57.2%) began receiving pocket money between the ages of 8 and 12. At this stage of development, children are already capable of developing basic financial skills through practical experience – deciding whether to spend or save, comparing prices, and planning expenses. An important aspect of financial independence also involves making decisions about borrowing and repaying money.

The most effective way to acquire these skills is undoubtedly through personal experience, rather than merely receiving advice from adults.

In contemporary times, a noticeable shift has been observed in the form in which pocket money is provided. According to the report “Finanse młodych Polek i Polaków” [Finances of young Poles] (Autopay, 2025), the share of cash is steadily decreasing in favour of increasingly popular digital payment methods. Only 9% of children aged 12–14 receive their pocket money in cash, while as many as 74% receive it in a digital form.

The Impact of Pocket Money on Saving and Spending Planning Among Youth

Regular receipt of personal funds provides young people with the opportunity to make their first financial decisions, which can serve as a foundation for developing future personal budgeting skills. Pocket money enables adolescents to plan their expenditures independently, set priorities, and allocate funds toward specific goals. However, the ways in which young people manage their money vary considerably. The formation of financial habits in individuals controlling their own funds is influenced by multiple factors, including parental relationships and the household’s economic situation (Lozza, 2023).

Findings from the conducted survey reveal a heterogeneous attitude among youth toward saving and expenditure planning. When asked, ‘Have you saved a portion of your pocket money?’ the majority of respondents (133 individuals) answered affirmatively, indicating a relatively strong propensity to save part of their received funds. Similar patterns were observed concerning larger financial objectives, such as purchasing electronic devices or financing a vacation, with 122 respondents reporting that they had set aside pocket money for specific goals. Notably, among those attempting to achieve larger financial objectives, most (93 respondents – 51.6%) successfully reached their intended outcomes.

The survey also investigated how respondents managed their funds. Only 71 participants reported planning their expenditures, whereas 109 admitted to spending spontaneously. This suggests that, despite a relatively high proportion of young people engaging in saving behaviours, systematic budget planning is not yet widespread.

Furthermore, nearly half of the respondents (97 individuals – 53.8%) indicated that they had experienced situations in which they ran out of money before receiving their next ‘pocket money’ payment. This finding underscores that, despite intentions to save and plan, many adolescents face challenges in balancing their expenditures with available funds. These difficulties may stem both from the limited amount of pocket money and from insufficient financial discipline.

The results of other studies on the impact of pocket money on saving and expenditure planning among young people are also inconclusive. The relationship between parental economic socialisation practices and the development of desired financial behaviours in children, such as expenditure control, is not statistically significant, according to Roszkowska-Hołysz (2018). The study indicated a weak positive correlation between regularly receiving pocket money and the propensity to save. The strongest tendency to spend money immediately was observed among individuals who received pocket money irregularly during childhood, whereas those who intended to save were predominantly respondents who had not received pocket money at all. Moreover, 82% of individuals who never received pocket money reported that managing expenditures posed no difficulty (Roszkowska-Hołysz, 2018).

Respondents’ opinions regarding the influence of pocket money and family financial socialisation were also varied. When asked, ‘Have you discussed your expenses with your parents or guardians?’ 94 individuals answered affirmatively. This suggests that, in many cases, knowledge of money management may develop more through personal experience than through family discussions. Most respondents (103 out of 180) do not regard their parents as an authority on financial matters. This finding may indicate young people’s pursuit of greater financial independence and autonomy in decision-making, as well as a weakening of parents’ role in their children’s education in economic matters.

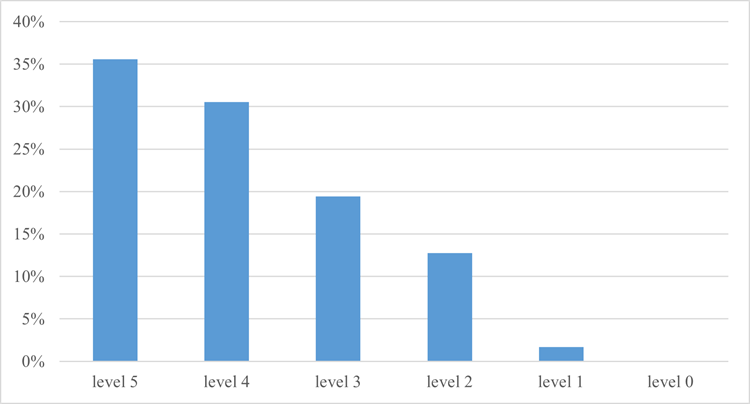

The results were somewhat more positive regarding parental guidance on money management and the impact of pocket money on the development of positive character traits. More than half of the respondents (105 out of 180) reported receiving advice from parents or guardians on managing money. Parents, therefore, often act as advisors, even if adolescents do not always perceive them as an authority in this area. The survey also included a question assessing the influence of pocket money on the development of positive character traits, such as patience, independence, and financial autonomy. Respondents evaluated this influence on a scale from 0 (no influence) to 5 (very strong influence). The results are presented in Figure 3.

Figure 3Do you think pocket money influences the development of positive character traits – for example patience or financial independence? (0 – no influence at all, 5 – very strong influence)?

Source: authors’ own work.

Based on these data, the average rating was 3.9. Thus, the majority of respondents perceive pocket money as positively impacting the development of beneficial, constructive personal traits, such as patience and independence.

Perceived Financial Risks and Challenges

Although pocket money plays an important role in economic education and can foster the development of positive financial attitudes, it is not without certain risks and educational challenges. The way in which young people manage their funds depends on factors such as family financial behaviour patterns, individual personality traits, and prior experiences. A lack of proper support or supervision may lead to undesirable outcomes, such as impulsive spending, poor budget planning skills, or excessive focus on consumption. These risks become particularly relevant in the context of new financial products, such as Buy Now, Pay Later (BNPL) schemes, which can increase the likelihood of entering a debt spiral early in adulthood.

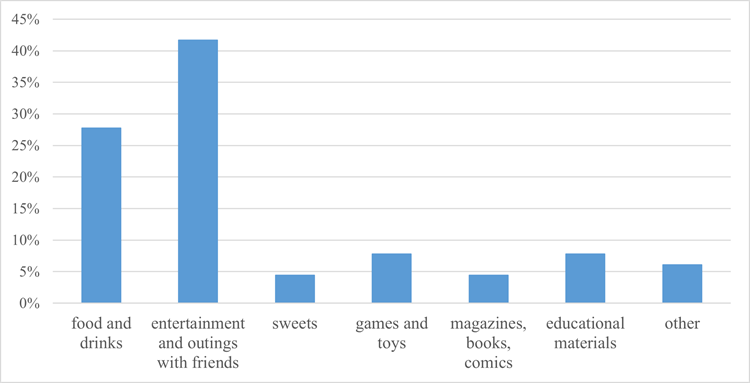

An analysis of responses to the survey question (Figure 4), ‘What did you most often spend your pocket money on?’ indicates that entertainment and social outings with friends were the dominant expenditure category (75 respondents – 41.6%), followed by food and beverages (50 respondents). Other categories – such as games and toys, educational aids, magazines, books, or sweets – were reported much less frequently. These findings suggest that adolescents primarily use pocket money for social and consumptive purposes, while allocating less of it toward personal development or educational activities.

Figure 4What did you most often spend your pocket money on?

Source: authors’ own work.

When asked whether the amount of pocket money could become a source of peer comparison or negatively affect well-being, as many as 133 respondents acknowledged that such a risk exists. A slightly lower, yet still noticeable, level of risk was associated with potential conflicts between the child and parents arising from the amount of pocket money – 103 respondents considered this situation possible. The greatest concern, however, was whether regular pocket money, combined with limited parental supervision, might foster negative habits, such as unhealthy eating or substance use. In this category, 151 respondents (levels 3–5) indicated that there is a real risk of such behaviours occurring. Students thus recognise both educational and social risks associated with pocket money. The majority believe that giving children money can only produce positive effects if accompanied by appropriate support, discussion, and parental oversight.

The scientific literature frequently emphasises that pocket money, despite its educational function, may be associated with certain risks to the health and well-being of young people. Research by Ma et al. (2020) showed that children who receive regular pocket money are more likely to consume unhealthy products and sugary drinks, with higher amounts of money positively correlating with increased rates of overweight and obesity. Gotwald (2022) highlights that, in addition to the risk of overweight, children’s financial autonomy may also be linked to poorer psychological well-being, including depressive symptoms (see Xiao et al., 2022). Similar associations are reported by Lozza (2023), who notes that access to money among adolescents increases the likelihood of engaging in risky behaviours, such as alcohol consumption, smoking, and gambling. Lozza emphasises that studies on Italian youth clearly show a relationship between the amount of pocket money and a greater propensity to use substances, as well as more frequent participation in out-of-home consumer activities.

Summary and Discussion of Research Results

The conducted study and literature analysis indicate that pocket money represents an important, though not unequivocal, element of young people’s economic education. For many students, it served as the first tool for developing financial independence, learning to plan expenditures, and setting aside funds for specific goals. The survey results confirm that most respondents express only a tendency to save and perceive pocket money positively, as a means of fostering traits such as responsibility and independence. However, the reality reflects the actual financial situation of Polish students. Young people generally receive small amounts from their parents, which are mostly spent on entertainment and social activities with friends.

At the same time, a relatively large number of respondents admitted that planning expenditures and maintaining financial balance remain challenging, indicating a need for further support in developing financial discipline. The risks and potential drawbacks associated with giving pocket money should not be overlooked, including peer comparison, conflicts with parents, and the development of undesirable consumption habits. These findings highlight the importance of parental involvement and financial education, grounded in knowledge of financial institutions and a clear understanding of household budget management principles.

References

- Autopay. (2025). Finanse młodych Polek i Polaków [Finances of young Poles]. https://www.scribd.com/document/914607829/Raport-Finanse-Mlodych-Polek-i-Polakow

- Bucciol, A., & Veronesi, M. (2014). Teaching children to save: What is the best strategy for lifetime savings? Journal of Economic Psychology, 45(1), 1–17. https://doi.org/10.1016/j.joep.2014.07.003

- Furnham, A. (1999). The saving and spending habits of young people. Journal of Economic Psychology, 20(6), 677–697. https://doi.org/10.1016/S0167-4870(99)00030-6

- Gotwald, B. (2022). Kieszonkowe – narzędzie edukacji finansowej czy czynnik ryzyka chorób cywilizacyjnych [Pocket money – financial education’s tool or a risk-factor of civilization diseases]. Akademia Zarządzania, 6(4), 256-277. https://doi.org/10.24427/az-2022-0066

- Laily, N. (2016). The influence of financial literacy on student behavior in managing finance. Journal of Accounting and Business Education 1(4).

- Lozza, E, Jarach, C. M., Sesini, G., Marta, E., Lugo, A., Santoro, E., Gallus, S., HBSC Lombardy Committee 2018; members of the HBSC Lombardy Committee 2018. (2023). Should I give kids money? The role of pocket money on at-risk behaviors in Italian adolescents. Annali dell'Istituto Superiore di Sanita, 59(1), 37-42. https://doi.org/10.4415/ANN_23_01_06

- Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. https://doi.org/10.1257/jel.52.1.5

- Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial literacy among the young. Journal of Consumer Affairs, 44(2), 358–380. https://doi.org/10.1111/j.1745-6606.2010.01173.x

- Ma, L., Fang, Z., Gao, L., Zhao, Y., Xue, H., Li, K, & Wang, Y. (2020). A 3-year longitudinal study of pocket money, eating behavior, weight status: the childhood obesity study in China mega-cities. International Journal of Environmental Research and Public Health, 17(23), 9139. https://doi.org/10.3390/ijerph17239139

- Mandell, L., & Klein, L. S. (2009). The impact of financial literacy education on subsequent financial behavior. Journal of Financial Counseling and Planning, 20(1), 15–24. https://psycnet.apa.org/record/2009-19876-001

- Novianti, I. D., & Kurnia R. A. (2023). The effect of financial knowledge and financial planning on financial skills with pocket money as a moderating variable in Generation Z (Case study on students of the Faculty of Economics and Business, University of Muhammadiyah Surakarta). International Journal of Social Science and Economic Research, 8(3), 532-547. https://doi.org/10.46609/IJSSER.2023.v08i03.014

- OECD. (2016). OECD/INFE international survey of adult financial literacy competencies. OECD Publishing. https://www.oecd.org/content/dam/oecd/en/publications/reports/2016/10/oecd-infe-international-survey-of-adult-financial-literacy-competencies_fe88832b/28b3a9c1-en.pdf

- Piekut, M. (2018). Zmiany w wydatkach na kieszonkowe w polskich gospodarstwach domowych [Changes in spending on pocket money in Polish households]. Handel Wewnętrzny, 4(375), 291-300. https://bazekon.uek.krakow.pl/rekord/171529686

- Roszkowska-Hołysz, D. (2018). Socjalizacja ekonomiczna a wybrane zachowania ekonomiczne dorosłych [Economic socialization vs. selected economic behavior of adults]. Ekonomia XXI Wieku, 3(19), 37–52. https://doi.org/10.15611/e21.2018.3.03

- Shim, S., Barber, B. L., Card, N. A., Xiao, J. J., & Serido, J. (2010). Financial socialization of first-year college students: The roles of parents, work, and education. Journal of Youth and Adolescence, 39(12), 1457–1470. https://doi.org/10.1007/s10964-009-9432-x

- Webley, P., & Nyhus, E. K. (2006). Parents’ influence on children’s future orientation and saving. Journal of Economic Psychology, 27(1), 140–164. https://doi.org/10.1016/j.joep.2005.06.016

- Xiao, Y., Chow, J., Han, K., & Wang, S. (2022). Expenditure patterns among low-income families in China: Contributing factors to child development and risks of suicidal ideation. Journal of Community Psychology, 51(2), 560-583. https://doi.org/10.1002/jcop.22826

https://orcid.org/0000-0002-6916-0761

https://orcid.org/0000-0002-6916-0761